Andrew White

Reveal Menu

Investment Commentary: Monthly Bulletin October 2017

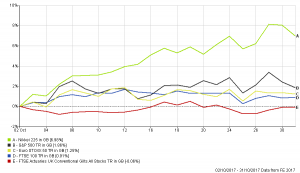

October proved to be a positive month for markets, but in reality, they simply reversed their previous month’s loss and failed to move materially higher. The performance of some of the main indices are shown below:

(all figures are based on bid to bid prices with income reinvested, in Sterling terms)

The main exception to this was Japan, where markets reached a twenty-year high on the back of President Abe’s landslide election victory, which increased expectation for a continuation of significant monetary stimulus.

This is in stark contrast to much of the remaining developed world where the rend continues to be one of policy tightening. Within Europe, the European Central Bank announced it was to halve its monthly stimulus to €30 billion and as we write this commentary the Bank of England’s Monetary Policy Committee have announced the first interest rate increase in over a decade.

America, who are further ahead in the process of winding down their stimulus (with two rate rises already this year), have announced Jerome Powell will replace Janet Yellen as Chairman of the Federal Reserve and it will be some time before we fully understand what his approach to managing the world’s largest economy will be.

Despite being cognisant of this back-drop, we must emphasise the reasons Central Banks feel confident to being the tapering process, which is that economies, generally, are beginning to look in better shape across the globe.

As a consequence we retain our positive attitude towards Equities, particularly in favour of other assets such as Bonds, remaining overweight in both UK and Globally, with an expectation for 2017’s positive momentum to carry on.

Pleasingly, this is a position that has helped all portfolios outperform relative to their Benchmarks over the year and this trend continued though October.

The Boolers Investment Comittee